Featured

Table of Contents

Even if you aren't stressed over rising rates, the longer you bring financial obligation, the costlier it is, the more discouraging it can be, and the harder it is to accomplish other objectives. Starting a brand-new year owing money can take a mental toll. No matter your exact scenarios, it's worth getting out of some debt in 2026 by pursuing alternatives like credit card debt relief or repayment using the debt snowball or financial obligation avalanche methods.

That can help you understand what you owe and how much you can genuinely afford to pay toward ending up being debt-free. Look at your bank and credit card statements to track your spending. Utilizing a budgeting app might be valuable here to see precisely how much of your money is going to fundamentals like groceries and bills, and how much is going to non-essentials like eating out or film tickets.

Research alters to legal rules: For example, in 2025 through 2028, automobile loan interest will be tax-deductible for qualified people as a result of provisions in the One Big Beautiful Costs Act. Using the information you collect, identify the following: Total impressive debtBalance of each financial obligation, and the interest rate you are being chargedWhether interest for each is tax-deductible (keeping in mind that the rules can alter over time, so checking once again in future is smart)Due date for regular monthly paymentsFunds you could use towards financial obligation reward Getting organized provides you a clear image of where you stand, what time frame for financial obligation payoff is sensible, and what debt relief options deserve pursuing.

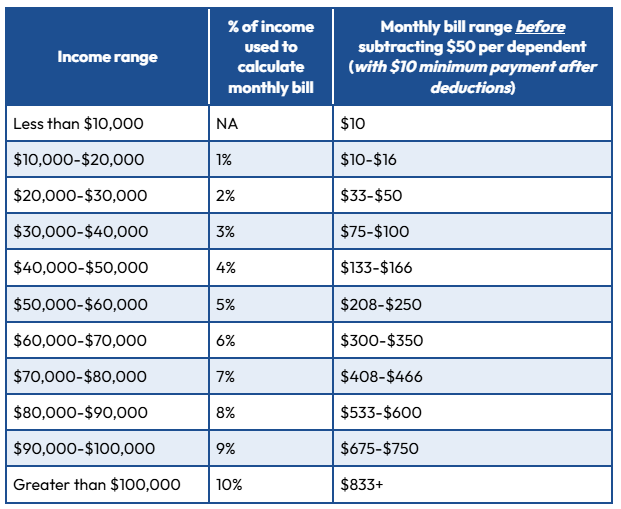

Federal State Financial Assistance Options for 2026

The two primary approaches are the financial obligation snowball and the financial obligation avalanche. Involves lining up your financial obligations from smallest to largest, and dealing with the smallest financial obligation. You continue this method with all your debts until you've paid whatever off.

State you have $200 of discretionary income in a month, and $10,000 of credit card financial obligation across five charge card. Pay the minimum payments on all 5 charge card, however allocate as much of that $200 as you can to paying off the credit card financial obligation with the smallest balance.

A huge benefit of the financial obligation snowball approach is that you pay off your first financial obligation quickly, which might help motivate you to remain on track. Andr Small, a qualified monetary organizer based in Houston, Texas and founder of A Small Investment, states much of his low-income customers prefer the snowball method, while individuals with more discretionary income may be inclined to utilize the financial obligation avalanche.

Similar to the snowball, make at least the minimum payment for all of your cards, with additional money going to the card with the highest APR (yearly portion rate). That very first debt you pay off might not have the tiniest balanceit could even have the highestbut this technique saves you money in interest over time vs.

Consolidating Unsecured Debt Into a Single Payment in 2026What Debt Strategy Is Best in 2026

That's because you since off the costliest debt. You may not score quick wins with this approach, so it might not be the best one if you think you'll have a hard time to stay inspired. Sometimes, simply making additional payments is not adequate to assist you become debt-free in an affordable amount of time.

MethodCostTime to FinishCredit ImpactHow it WorksBest ForDebt management planTypically under $50/month3 -5 yearsYesA nonprofit credit therapy firm works out a payment strategy for all of your unsecured debtFull debt payment with professional finance guidanceDebt ConsolidationVariesVariesYesYou take a brand-new loan to repay numerous existing financial obligations. Lowering your rate (if you receive more affordable funding)Balance Transfer3-5%VariesYesYou transfer existing credit card financial obligation onto a new card with 0% balance transfer deal.

Most unsecured financial obligations are qualified to be forgiven Chapter 13 includes a 3- to five-year repayment plan. Borrowers who require legal protection from creditorsEach option has pros and cons. Here's a little bit more information about how each works: Financial obligation debt consolidation: If you receive a debt consolidation loan, this can be a fantastic choice.

This streamlines things, considering that you have only a single payment. Depending on whether you make your loan term longer or much shorter, it could likewise lower overall loaning expenses, as long as you aren't paying for a lot longer than you were on the loans you combined. Financial obligation settlement: You or a financial obligation relief company negotiate with creditors and get them to accept a lump amount payment or payment strategy for less than the full amount you owe.

Starting the New Bankruptcy Legal System

Credit therapy: You deal with a certified therapist to examine your financial resources and figure out how much you can pay toward financial obligation. Credit therapists provide monetary counseling when you enroll in a debt management strategy. That's a structured payment program in which you make one monthly lump amount payment, which money is distributed to creditors by the financial obligation management company based upon terms they've worked out.

Usually, there is a cost of around 3% to 4% to do the balance transfer. Sadly, you generally have only a brief time at the 0% rate, so it's easy to fail to end up being debt-free utilizing this approach. After the promotional period, the rates go up to the much greater rates common of charge card.

With Chapter 13 insolvency, you participate in a three- to five-year payment agreement and must satisfy the repayment strategy before any financial obligation is forgiven. Liberty Financial obligation Relief can work out financial obligation settlement on your behalf if you choose this is the best technique. Typically, you make a month-to-month deposit into a devoted account (that you own and manage).

Once the lender has accepted a settlement and you approve it, payment is made from your devoted account. When the terms of the contract are satisfied, the debt is behind you and you do not have to stress over it again. Financial obligation relief programs make debt benefit easier, however you need to certify to take part.

Proper Ways to Manage Persistent Creditors

Unsecured debt: Lenders don't typically settle safe financial obligation (debt for which there is collateral ensuring the loan). As an outcome, your debt must be unsecured to take part in a lot of expert financial obligation relief programs. Proof of financial challenge: You must be dealing with difficulties paying your costs, and may require evidence of monetary hardship, such as evidence of a job loss or income decrease.

Financial obligation settlement can't remove your debts entirely. You can reach out to get a complimentary financial obligation examination to find out if you certify for the Freedom Debt Relief program.

{kind=link}

Latest Posts

Official Federal Debt Relief Initiatives in 2026

Choosing Between Bankruptcy and Debt Settlement Options

Selecting Reliable Debt Settlement Services in 2026